The Central Economic Administrative Tribunal (TEAC) in unification of criteria, has established that the freedom of amortization is considered as an option for the taxpayer. Read on and we’ll tell you the reasons.

Application of the freedom of depreciation

An entity submits its Corporate Tax return for the 2013 financial year without applying any adjustment for freedom of amortization. Upon receipt of a request in order to verify whether it had properly applied the 70% depreciation limitation provided for in 2013 and 2014, it decides at the stage of processing allegations and settlement proposal, to request the realization of a negative extra-countable adjustment to apply the remainder of the depreciation freedom not applied in previous years, and in this way , mitigate the increase in the tax base revealed by the Tax Administration.

This request is not accepted as the Tax Administration understands that the application of the freedom of amortization is an option. The same applies when it lodges an appeal for reinstatement. However, the TEAR of Cantabria, does give the reason, to understand that the adjustment for freedom of amortization is not an option, but the exercise of a right, which the taxable person can exercise within the limitation period or expiration, being able to exercise it in the regularization that in his case occurs within a verification procedure.

Before the resolution of the Regional Economic Administrative Court (TEAR) of Cantabria, the Director of the Inspection Department of the Tax Agency (AEAT) files an extraordinary appeal for the unification of the criterion, and to determine if the freedom of amortization is an option and, consequently, when it can be exercised.

In this regard, the Central Economic Administrative Court (TEAC), based on the doctrine established by the Supreme Court on options, considers that the freedom of amortization is an option and its exercise can only be carried out within the regulatory period of submission of the declaration. Thus, if a taxpayer decides in the declaration of an exercise not to apply the freedom of amortization to certain assets and / or rights, subsequently it can no longer change that option with respect to that exercise. The foregoing does not prevent you from enjoying the benefit in subsequent years, even if the freedom of amortization reaches the same assets and /or rights.

Thesame sense has been expressed by the TSJ Galicia 13-6-17 and the DGT CV 18-4-16.

Concept of freedom of depreciation

With the expression ‘freedom of amortization’ can refer to the absence of any of the legally established methods, to the systems specifically included in the corporate tax rule, or to the practice of amortization contained in certain special rules:

- (a) Depreciation on the basis of proof of effectiveness. The regulations leave open to the taxpayer the freedom to adopt any method of amortization that includes an effective depreciation different and higher than that resulting from the legally established methods. It requires proofin each case by the taxpayer of that effectiveness.

It is clear that it is a theoretical rather than a real possibility, due to the very difficulty of the test. However, it may be admitted when the actual wear and tear is individually proven, even if accreditation is not possible by means of general criteria.

- b) The regulations of corporation tax regulate a regime of freedom of amortization for certain investments,whatever the investment entity, as well as for investments made by certain entities. It also contains a special scheme for job-creating investments by small firms.

Freedom of repayment

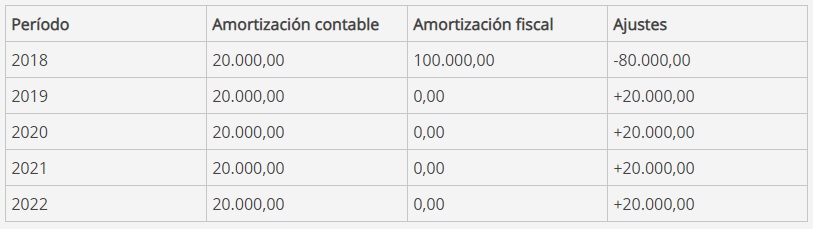

1) An item that is purchased on January 1, 2018 for 100,000 u.m., amortizable by tables at the maximum coefficient of 20%, enjoys freedom of amortization.

The accounting and tax depreciation would be as follows:

2) A company enjoys freedom of amortization and makes an investment at the beginning of 2018 of 80,000.00 amortizable according to the amortization table at the coefficient of 10%. The company makes use of the freedom of amortization in the tax period in which it makes the investment. At the beginning of 2021 it disposes of the item for 50,000.00.

The sequence of accounting and tax expenditures and adjustments is as follows:

At the beginning of 2021 the book value of the item is 56,000.00 (80,000.00 – 24,000.00), so in the sale an accounting loss of 6,000.00 is obtained. However, for the purpose of determining the tax base for that period, it should be taken into account that the amounts applied to the freedom of depreciation reduce, for tax purposes, the value of the amortized elements, so that a positive adjustment will have to be made to the accounting result for the amount of the negative adjustment made in 2018 that is pending inclusion in the tax base , that is, the positive adjustment to be made amounts to 56,000.00 (72,000.00 – 16,000.00).

What do I freely amortize?

If your company can apply the depreciation freedom and you have several assets on which to do so, apply it to those with a lower depreciation ratio.

Small size

Your company applies the regime of small companies and, as it has made investments in new assets and has increased its workforce, it will apply the incentive of freedom of amortization.

If you have several assets to apply to, do so on those with a lower depreciation ratio. The deferral in the payment of Corporation Tax will be greater and you will obtain more financial savings.

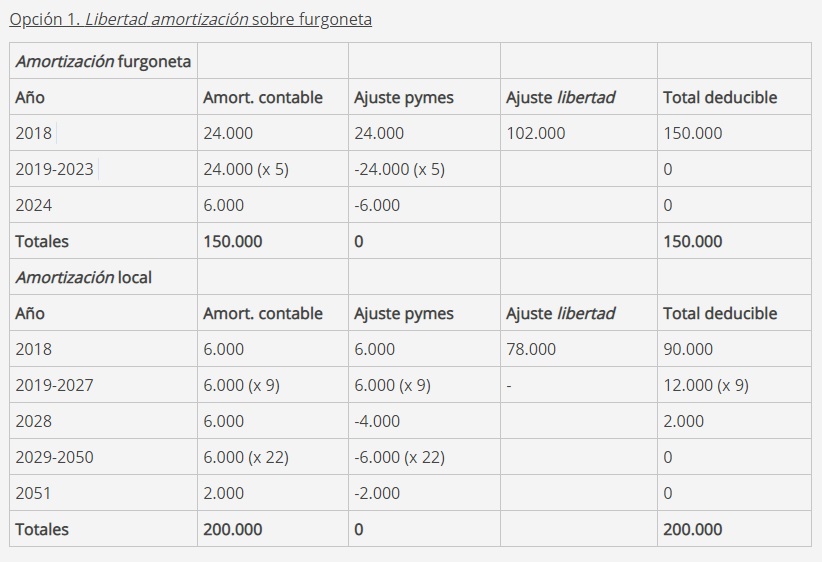

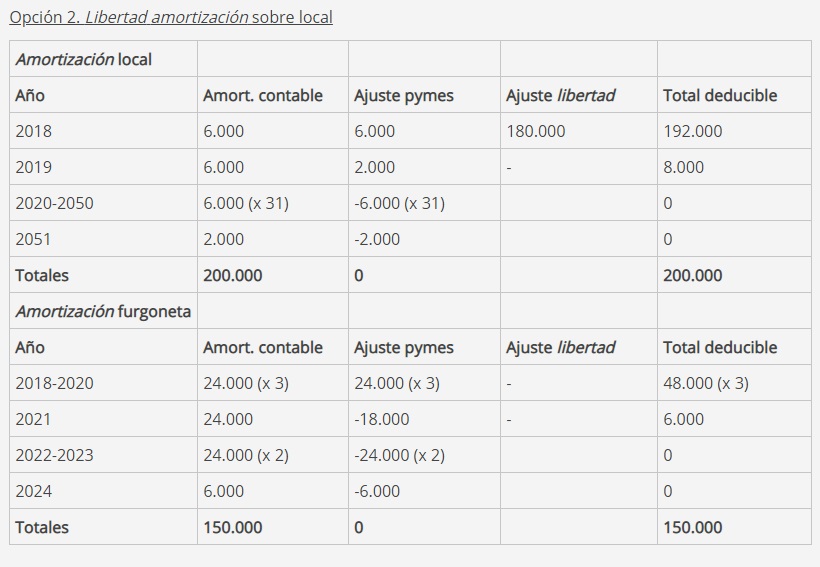

An example: On January 1, 2018 your company acquired five new vans for a total of 150,000 euros (amortizable at 16% per year). On the same date it acquired a new premises with an amortizable value of 200,000 euros (which is amortized at 3% per annum).

If you increase your workforce by 1.5 workers (which will allow you to freely amortize 180,000 euros), these are the adjustments to be made:

Financial savings

Option 2 allows for higher fiscal spending during the first few years, which translates into greater financial savings.

Considering an interest rate of 6%, the savings derived from option 2 will be 16,003 euros, compared to 11,793 euros in option 1. A difference of 4,210 euros that should be taken advantage of.

Remember that the freedom of amortization is compatible with the accelerated amortization of SMEs, so you can apply both incentives on the same asset.

Freely amortizing assets with a lower depreciation ratio allows for more financial savings.

If you have any questions or need any clarification about this type of TEAC criteria, you can contact our advisors to help you resolve them.